Moving to Japan is an amazing adventure. But setting up your new life can sometimes feel like a puzzle. You go to rent an apartment, and they ask you for a local phone number. You go to get a phone number, and the shop asks for a Japanese bank account. Then you go to open a bank account, and the bank clerk asks for your phone number!

This is called the "Phone-Bank-Address Loop." It frustrates thousands of new arrivals every year.

The good news? You can break this loop easily. This guide will show you exactly what to prepare, which bank to choose, and how to get approved on your very first try.

Quick Summary

To open a bank account in Japan as a foreigner, you need a Residence Card with your current address printed on it, a valid passport, and a real Japanese voice phone number to receive text verification codes. Japan Post Bank (Yucho) is the easiest and fastest choice for people who have lived in Japan for less than six months.

Step 0: How to Break the Phone Number Loop First

Most traditional guides tell you to go to the bank first. That is outdated advice. In 2026, Japanese banks have incredibly strict security rules to stop fraud.

Because of this, almost every Japanese bank makes you provide a Japanese phone number during the application. The bank's computer system will send an SMS verification (text message) verification code to your phone while you are sitting at the desk or using their web form. If you cannot type that code in immediately, the bank may reject your application.

Here is the catch: You cannot use a data-only travel eSIM or tourist SIM card. These temporary cards do not have a real Japanese voice line, so they cannot receive security verification texts from banks.

You must secure a real voice phone plan before visiting a bank branch. Foreigner-friendly services like Sakura Mobile solve this perfectly. You can order a Voice SIM or eSIM online using your passport before setting up your banking. They accept international credit cards and provide a fully compliant Japanese phone number, letting you pass the bank's safety checks easily.

The 2026 Document Checklist

Before you walk into a bank branch, you must gather your paperwork. If your documents are missing even one thing, the bank will turn you away.

Use this general checklist to make sure you have everything ready:

| What You Need | Why It Matters | What to Double Check |

|---|---|---|

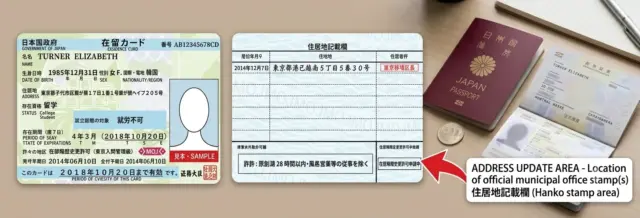

| Residence Card (Zairyu Card) | This is your official ID in Japan | Your current home address must be officially printed on either the front or the back of the card. |

| Passport | It proves who you are | Make sure it is not expired! |

| Japanese Phone Number | The bank uses this to text you security codes and identity verification | It must be a real number that can receive standard texts (no internet-only numbers). |

| School or Job Proof | It proves why you are in Japan | If you are a student, bring your student ID. If you work, bring your job contract. |

| Cash for Your First Deposit | This is often required to activate your account | Bring at least 1,000 yen in cash to put into your new account right away. |

⚠️ The Middle Name Mistake: Japanese computer systems are very rigid. If your passport says Jonathan Michael Smith but your Residence Card lists you as Smith Jonathan M., the bank's system will flag it as an error. Always type your name exactly how it looks on your physical Residence Card. Match the word order, the initials, and the spaces perfectly.

Please Note: Every bank has its own set of rules, and the exact papers they ask for can sometimes change. To avoid any surprises, always double-check the official website of the specific bank you choose before you head out!

Which Bank is Best for You?

Not all Japanese banks treat visas equally. Megabanks often have strict rules for foreigners. Here is a simple look at your best options in 2026.

| Bank Name | Best For | English Help | The Catch |

|---|---|---|---|

| Japan Post Bank | New arrivals, students, and fast setups. | Great (They have application forms written in English) | You cannot send or receive money from overseas during your first six months. |

| Sony Bank | People who like online banking and smartphone apps. | Full English apps and support | You must live in Japan for at least six months before they will approve you. |

| Big Megabanks (like MUFG or SMBC) | People whose jobs force them to use these specific banks. | Low (Staff usually only speak Japanese) | You must live in Japan for six months or have a formal work contract. |

Step-by-Step: How to Open a Japan Post Bank Account

Important 2026 Update: Japan Post Bank used to let new arrivals open accounts using a smartphone app. However, due to updated Residence Card designs released this year, all new foreign residents must now apply in person at a physical branch.

Follow these steps to ensure a smooth visit:

Register Your Address and Activate Your Phone

Visit your local city hall (ward office) to make sure your current address is officially registered on your Residence Card. Turn on your phone and ensure your Japanese voice line is active and capable of receiving texts and calls.

Fill Out the English Form Online

Go to the official Japan Post Bank website and look for the multi-langauge application page. Fill out your details in English on your computer or phone. The site will generate a custom paper form or a QR code. Print this out or bring it with you—it saves you from translating tricky Japanese forms at the bank counter.

Go to a Branch in Your Neighborhood Early

You must visit a bank branch in the exact same neighborhood where you live or work. This way, if you need to change things, it is more convenient for you. Also, Japanese banks close incredibly early!

Most banks close at 3:00 PM, but Japan Post Bank (Yucho) is slightly different. Some Yucho branches close at 3:00 PM, while others stay open until 4:00 PM. Arrive as early as possible to give the staff plenty of time to process your papers, and check your specific branch hours online first!

Verify Your Phone Number

Hand over your paperwork. The bank clerk will type your information into their system and send a live security code to your phone or call your number. You will walk out of the bank with a physical paper bankbook immediately. Your plastic cash card will arrive safely in your home mailbox 7 to 14 days later.

Two Hidden Rules You Should Know

The 6-Month Waiting Rule: Because of strict international money laws, if you have lived in Japan for less than six months, your account is legally labeled as a "Non-Resident Account." You can use it to deposit your paychecks or buy things inside Japan. However, you cannot send money back home or receive international wires until you hit your six-month anniversary.

The "Main Branch" Tie: In Japan, your account is permanently tied to the exact bank branch where you first opened it. If you lose your cash card, change your visa status, or need to fix a serious issue, many traditional banks stubbornly make you walk into that same exact building to sign the paperwork. If you open your account at a branch in Tokyo and then move to Osaka, changing your details can become a massive headache. Always pick a branch that is easy for you to visit regularly!

Ready to Check "Open a Bank Account" Off Your List?

Opening a bank account in Japan does not have to be stressful. As long as you register your address at the city hall, print your name exactly as it looks on your ID, and bring a working Japanese phone number to the counter, you will slide through the process easily.